ALL eyes will be on Reserve Bank of Zimbabwe Governor Dr John Mangudya, when he presents the 2026 Monetary Policy Statement tomorrow, with policy focus expected to shift from stabilisation to growth and sustainability.

Given the progress in curbing inflation, Zimbabwe’s monetary policy needs to continue to strengthen domestic currency stability, rebuild credibility and manage money supply to support sustainable economic growth.

But among the most poignant issues for captains of industry and commerce leaders ahead of the 2026 monetary policy presentation is the bank’s interest direction.

After a year marked by tight liquidity conditions, a 35 percent bank policy rate and exchange rate stability, businesses now want clarity on the next phase of the RBZ’s monetary policy trajectory, including when the central bank will begin easing and how far this would go.

Will it maintain a cautious stance to defend the gains made?

The central bank is on record saying it will not rush to introduce monetary easing without clear guarantees that the gains thus far, a remarkable inflation drop and exchange rate stability, will be protected.

Nonetheless, the expectation across business and financial markets is a review of the central bank’s benchmark policy rate.

The benchmark rate indicates the central bank’s desired interest rate level and the bank has thus maintained a tight regime since introducing the new currency in April 2024, to reduce inflation and stabilise the economy.

Inflation dropped to single-digit levels, 4,1 percent in January for the first time since 1997, while the premium between the parallel market and official exchange rates has narrowed from over 100 to less than 20 percent.

While the gains are enormous, business leaders and economic analysts have noted that the liquidity squeeze on businesses has been evident, weighing on competitiveness.

One thing is obvious, though: maintaining current stability will require a delicate balance between central bank easing and the current hawkish monetary stance to maintain downward pressure on inflation and support the value of the ZiG.

There is a need for the Treasury to maintain strict fiscal discipline, avoiding money printing for quasi-fiscal operations that could undermine the central bank’s stability efforts. In its submissions ahead of the policy presentation on Friday, one of the country’s most influential business lobby groups, the Zimbabwe National Chamber of Commerce (ZNCC), said, “The 35 percent policy rate has translated to ZiG lending rates of 40–47 percent, significantly constraining access to credit for productive sectors despite the Targeted Finance Facility (TFF)”.

ZNCC has projected the ZiG annual inflation rate to remain below 10 percent in 2026, from an estimated 18–20 percent in 2025 and suggested a possible strategic reduction in the nominal policy rate to 20 percent.

The business lobby group recommended retaining positive real interest rates while signalling a data-contingent, gradual easing path as inflation expectations stabilise.

Confederation of Zimbabwe Industries (CZI) Matabeleland Chapter president, Mr Steven Ncube, said industry acknowledged the stability achieved so far, but highlighted the impact of the policy stance on businesses.

“As the private sector, we commend both the fiscal and monetary authorities for the current macro-economic stability characterised by single-digit inflation and a stable exchange rate,” said Mr Ncube. “However, we urge the authorities to reduce interest rates at the appropriate time to support the productive sector.”

He noted that between January and November 2025, local currency loans accounted for just 11 percent of total commercial bank lending, with 89 percent denominated in US dollars — a sign that local currency credit remains subdued.

The CEO Africa Roundtable chief economist Mr Tatenda Nyachega, said a downward review of the policy rate would ease lending costs and enhance competitiveness.

“When you look at issues related to the banking rate, we firmly believe there is a need to review the policy rate downwards so that it also has a positive impact on lending rates,” said Mr Nyachega.

“The whole essence is to ensure that we remain competitive when compared to other countries in the SADC region.”Local US dollar lending rates, currently around 20 percent, remain significantly higher than regional peers such as Namibia and Botswana, placing domestic firms at a disadvantage.

However, expectations are tempered by caution. The business group also warns that any premature relaxation, particularly without adequate foreign exchange reserves, could reignite volatility.

Investment analyst, Mr Tafara Mtutu, said he expected liquidity in ZiG to remain tight. He said, “Even if the central bank trims rates, they are likely to remain above US dollar levels to keep the lid on speculative borrowing”.

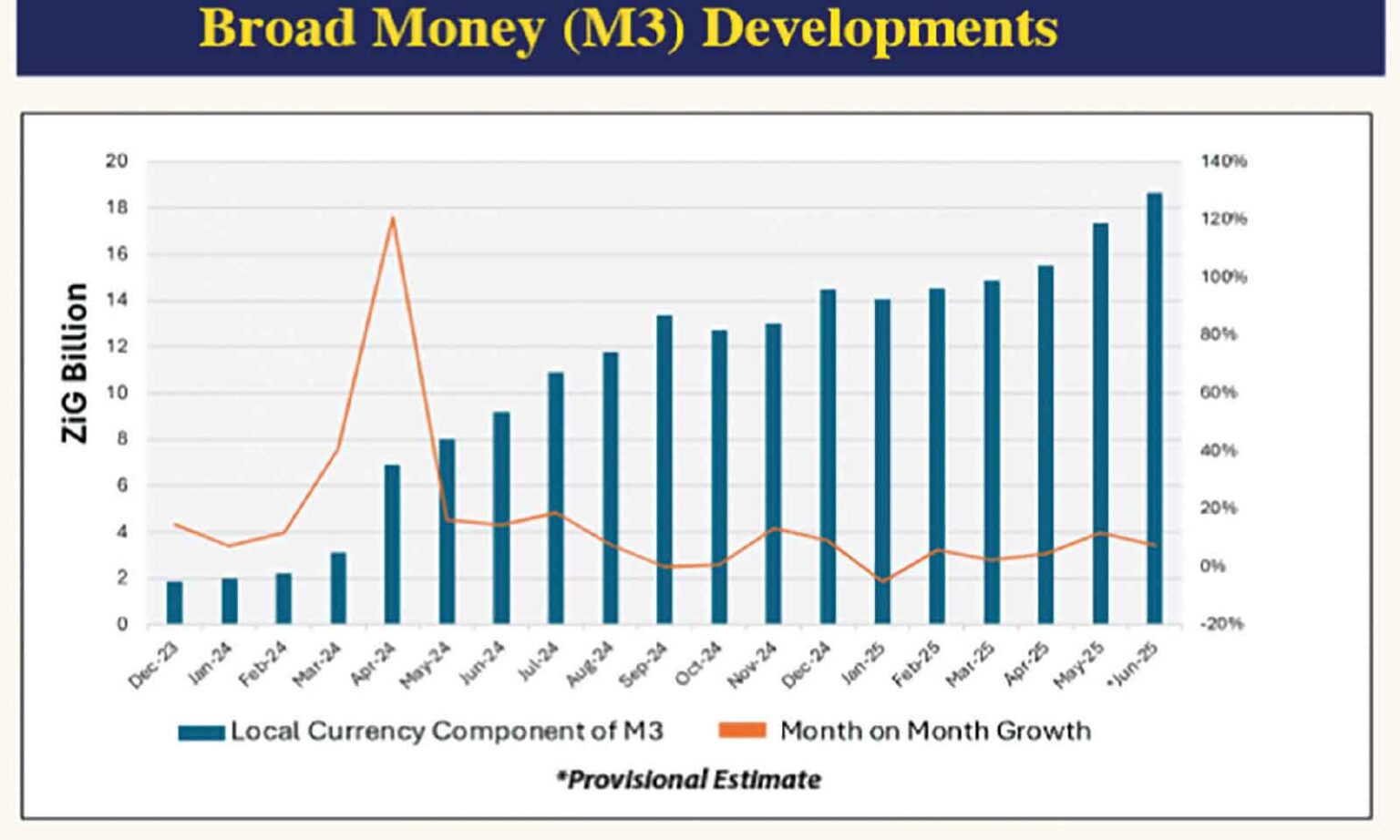

Economist Mr Enoch Rukarwa believes interest rates are only one part of the equation. He says that the current ZiG money supply, estimated at around 16 to 18 billion and accounting for roughly 15 to 16 percent of total liquidity, is insufficient to support any meaningful transition towards de-dollarisation.

“At these levels, already transactions in ZiG are stifled because the volume of the ZiG notes is not sufficient,” said Mr Rukarwa.

He also called for the introduction of higher-quality ZiG notes, noting that those in circulation wear out quickly as usage increases.

For small and medium enterprises, the stakes are particularly high.

Mr Farai Mutambanengwe, President of the SME Association of Zimbabwe (SMEAZ), said the 35 percent policy rate basically locks away funding, especially in an environment where inflation has stabilised.

“That policy rate has to come down to be more or less aligned to the same interest rate as the US dollar,” said Mr Mutambanengwe.

He also called for a shift towards a completely market-driven exchange rate across the economy, arguing that the current dual structure makes it difficult for SMEs to access foreign currency through formal channels.

“If we have a market exchange rate, then it means that as an SME, when I apply for foreign currency, the process happens quickly and it’s not cumbersome,” he said.

Beyond interest rates, SMEs want action on bank charges and the Intermediated Money Transfer Tax (IMTT), which they say increases transaction costs and discourages use of formal banking systems.

The ZNCC submissions echo these concerns, recommending that authorities reduce bank charges and enforce transparency on non-funded income.

Another delicate issue the governor must address is confidence in the ZiG.

ZNCC’s 2025 industry survey also found that 76 percent of businesses believe macroeconomic conditions are not yet adequate to support full de-dollarisation, while 84 percent prefer either the US dollar or a multicurrency regime. It is expected that Friday’s monetary policy statement, the first of the next five towards Zimbabwe’s dedollarisation deadline of 2030, will give an overview of progress and policy framework towards key targets.

Notably, the central bank has said a series of key economic fundamentals must be fulfilled before the transition to a domestic mono-currency regime, a key requirement to accelerate growth and drive local competitiveness. ZNCC cautions, “De-dollarisation should be earned through sustained stability, not legislated through compulsion”.

As such, analysts say authorities must focus on creating conditions for a successful transition, such as ensuring low inflation and a sound financial system, rather than administrative bans on foreign currency.

They will also need to work on measures to encourage greater acceptance of ZiG in the informal sector, which accounts for a large portion of the economy, to reduce reliance on the US dollar, which still dominates transactions.

The central bank will also need to implement a structured, gradual phase-out of US dollar-denominated loans and contracts by 2030, ensuring business continuity.

Zimbabwe is expected to continue accumulating gold and foreign currency reserves to support the ZiG, to ensure it is backed by more than 100 percent of the reserves, thereby maintaining public trust.

Market watchers also say the central bank should shift focus to managing money supply (M3) to curb inflationary pressures, ensuring that the issuance of new ZiG notes corresponds strictly to the backing reserves.

Another significant expectation from the policy is the rollout of redesigned, high-quality ZiG banknotes and coins to improve durability and user-friendliness, addressing shortages in smaller denominations.-herald